Summary:

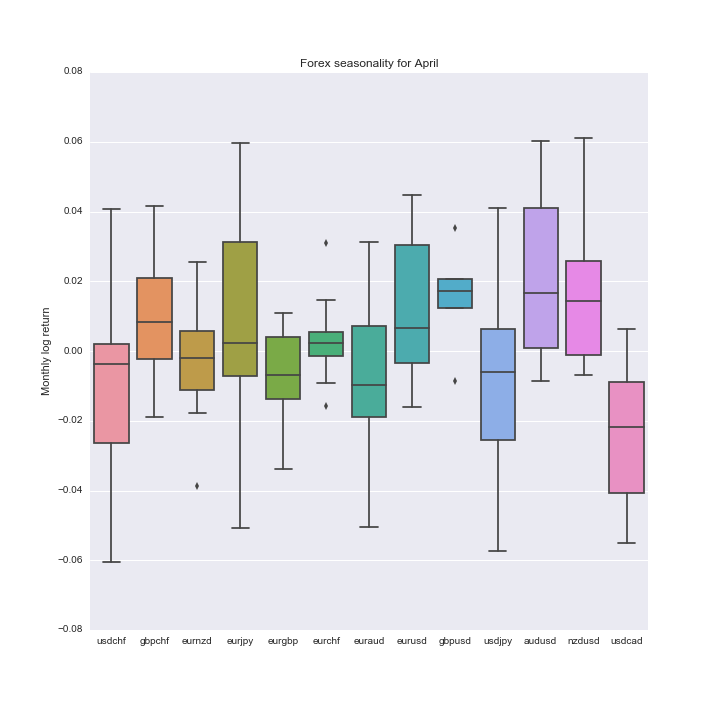

– In April, it’s typical to see the US Dollar decline; this year, the greenback has been weaker than seasonality suggests.

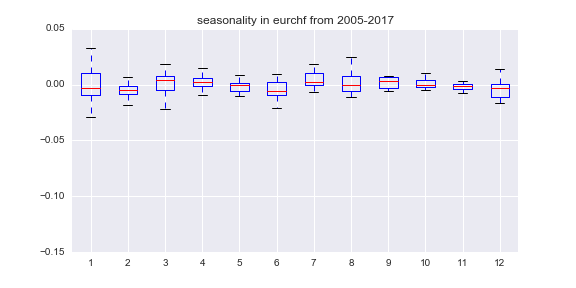

– DXY weakness, seasonally, can be attributed to its largest component, the Euro (57.6% of weighting).

-It’s expected to see an increase in commodity and energy prices, especially gold and oil.

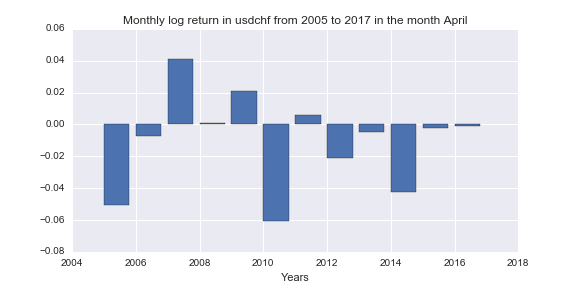

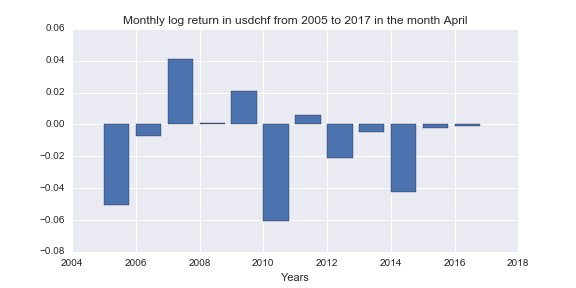

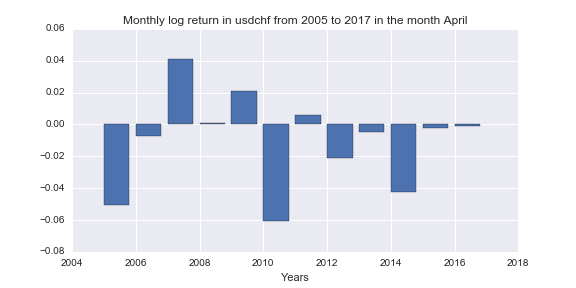

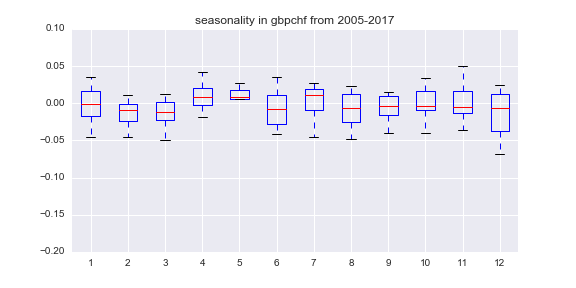

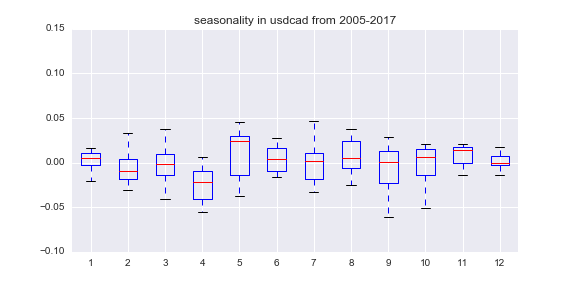

At the beginning of the month it’s time to review of the seasonal patterns that have influenced forex markets over the past decade. For April, we are going to investigate the period of 2005 to 2016 in recognition of the evolving relationship between economic data, central banks, and financial markets.

The longer observation period captures several crisis events/periods that traders may find analogous to events unfolding today, even as the ramifications from Brexit are unclear: the US tech bubble; the US housing bubble; the global commodity bubble; and previous rate hiking and rate cutting cycles, from the major central banks, during times normal (pre-2008) or extraordinary (post-2008).

As we can see for April, the dollar is pretty weak relative to other major currencies, this year, the greenback has been weaker than seasonality suggests since the market has priced in Fed March interest rate hike for the first time in 2017, the investors have digested the news and they are selling the fact now in the following month. It’s expected to see a weak dollar until next FOMC meeting.

It’s also expected to see an increase in commodity and energy prices, especially gold and oil. The currency behind gold and oil is Aussie and Loonie respectively. We see these two currencies are strong in April.